Essential Accounting Foundations for Startups

Launching a startup is exciting—but without strong accounting foundations, even the most promising business can run into cash-flow issues, tax problems, or operational roadblocks. Good accounting isn’t just paperwork; it’s the backbone of sustainable growth. At Clarus Accountancy Group, we help founders build solid financial systems from day one. This guide covers the essential accounting foundations every startup needs to succeed. ⭐ 1. Choose the Right Business Structure The first financial step for any startup is determining how you’ll legally operate.Choosing the wrong structure can affect your taxes, liability, and future funding options. Your main options are: Sole Trader – simple and quick to set up Limited Company – more tax-efficient and credible Partnership – suitable for co-owned businesses Why this matters: Your structure affects tax rates, legal protection, and how investors view your startup. Clarus can help you choose the right structure for your goals. ⭐ 2. Separate Business and Personal Finances Mixing personal and business money creates confusion, tax errors, and financial blind spots. Set up: A dedicated business bank account A business credit/debit card Clear transaction categories in your accounting software Benefits: ✔ Easier bookkeeping✔ Clean audit trail✔ Better visibility of startup finances ⭐ 3. Implement Cloud Accounting Software Modern accounting software gives startups real-time insights and automates repetitive tasks. Recommended platforms: Xero QuickBooks FreeAgent Sage Accounting What cloud accounting provides: ✔ Automatic bank feeds✔ Fast invoicing✔ Expense tracking✔ VAT calculation✔ Real-time reporting Clarus can set up your software and tailor it to your industry. ⭐ 4. Understand Your Key Financial Statements Every founder should know these three core reports: 1. Profit & Loss (P&L) Statement Shows profitability over time. 2. Balance Sheet Shows assets, liabilities, and financial health. 3. Cash Flow Statement Shows money entering and leaving the business. Understanding these reports helps you make informed decisions and track growth. ⭐ 5. Track Essential Financial KPIs Startups need measurable insights—not guesswork. Important KPIs include: Cash burn rate Gross profit margin Customer acquisition cost (CAC) Revenue growth Runway (months of cash remaining) Clarus can set up KPI dashboards so you can track performance at a glance. ⭐ 6. Keep Accurate Records from Day One HMRC requires accurate financial records. More importantly, clean records help you: ✔ Avoid penalties✔ Claim all allowable expenses✔ Prepare for investors or lenders✔ Forecast cash with confidence Records you should maintain: Invoices Receipts Contracts Payroll data Bank statements VAT records Asset purchases ⭐ 7. Manage Cash Flow Proactively Cash—not profit—is what keeps a startup alive. Improve cash flow by: Invoicing immediately Automating payment reminders Negotiating supplier terms Reducing unnecessary expenses Forecasting future cash needs Clarus provides detailed cash-flow forecasting tailored to startups. ⭐ 8. Understand Your Tax Responsibilities Tax mistakes can cripple an early-stage business.Startups must understand when and how to handle: Income Tax / Corporation Tax VAT registration PAYE & payroll Dividends & director salaries Allowable expenses R&D tax credits (if applicable) Clarus ensures full compliance and identifies tax-saving opportunities. ⭐ 9. Use a Professional Accountant as a Growth Partner Founders wear many hats—but accounting shouldn’t be one of them. A professional accountant helps you:✔ Avoid costly errors✔ Improve cash flow✔ Pay less tax✔ Make smarter decisions✔ Build investor-ready financials✔ Scale confidently ⭐ Final Thoughts Strong accounting foundations give startups the financial clarity they need to grow, hire, and secure investment. With the right systems and expert support, you can scale confidently and avoid the problems that cause early-stage businesses to fail. Clarus Accountancy Group supports startups with complete accounting, tax planning, forecasting, software setup, and strategic financial advice.

Limited Company vs Sole Trader: Which Is Right for You?

Choosing the right business structure is one of the most important decisions you’ll make as a business owner. It affects everything—from how much tax you pay to how protected you are legally. The two most common options in the UK are sole trader and limited company, each with its own advantages and responsibilities. At Clarus Accountancy Group, we help entrepreneurs, freelancers, and growing SMEs choose the structure that best supports their goals. Below, we break down the key differences so you can make an informed decision. ⭐ 1. What Is a Sole Trader? A sole trader is the simplest business structure. You and the business are legally the same entity. Key Features Easy and quick to set up Full control over the business Simple tax filing Minimal admin Pros ✔ Low cost and easy to start✔ Straightforward accounting responsibilities✔ Full control over profits✔ Flexible—ideal for freelancers and micro businesses Cons ✘ You are personally liable for all business debts✘ Higher tax rates once income grows✘ Harder to separate personal and business finances✘ May appear less credible to clients and lenders ⭐ 2. What Is a Limited Company? A limited company is a separate legal entity from you as the business owner. This provides stronger protection and more flexible tax planning. Key Features The business is legally independent Directors manage the company Profits belong to the company Must file annual accounts and Corporation Tax Pros ✔ Limited liability protects your personal assets✔ More tax-efficient at higher income levels✔ Professional and trustworthy appearance✔ Easy to scale and bring in shareholders✔ Pension and dividend planning benefits Cons ✘ More paperwork and compliance✘ More costs for accounting and administration✘ Public record filing at Companies House ⭐ 3. Tax Differences: Which Saves You More? Sole Trader Tax You pay Income Tax on profits You pay Class 2 & Class 4 National Insurance Fewer tax-planning options Limited Company Tax Company pays Corporation Tax on profits Owners pay themselves via: Salary Dividends (lower tax rate) More opportunities for: Pension contributions Expense claims Tax-efficient remuneration General rule: ➡ Sole trader is better for low income➡ Limited company becomes more efficient as profits grow Clarus Accountancy can calculate the most tax-efficient structure for your exact circumstances. ⭐ 4. Liability & Legal Protection Sole Trader: You are personally responsible for all debts. If the business fails, your personal assets—including your home—may be at risk. Limited Company: Your liability is limited to the company’s finances. This is one of the strongest reasons business owners choose this structure. ⭐ 5. Credibility & Growth Potential A limited company often appears more stable and professional, especially when seeking: Larger contracts Investment Business loans Partnerships Sole traders may find it harder to win corporate clients or scale quickly. ⭐ 6. Administrative Responsibilities Sole Trader Minimal admin Simple Self-Assessment tax return Limited Company Annual accounts Corporation Tax return Confirmation statement Payroll (if paying a salary) Dividend records Clarus Accountancy Group handles all limited company compliance, making the process stress-free. 🌟 Which Is Right for You? Choose Sole Trader if: You want a simple setup You are testing a new idea Your income is modest You prefer minimal admin Choose Limited Company if: You want better tax efficiency You want to protect your personal assets You are growing quickly You want to appear more professional You want flexibility in how you pay yourself ⭐ Final Thoughts Your business structure impacts your tax, credibility, finances, and future growth. There is no one-size-fits-all answer—but with expert guidance, you can make the right choice from the start. Clarus Accountancy Group can advise you on the best structure for your goals and handle all setup, accounting, and tax requirements so you can focus on growing your business.

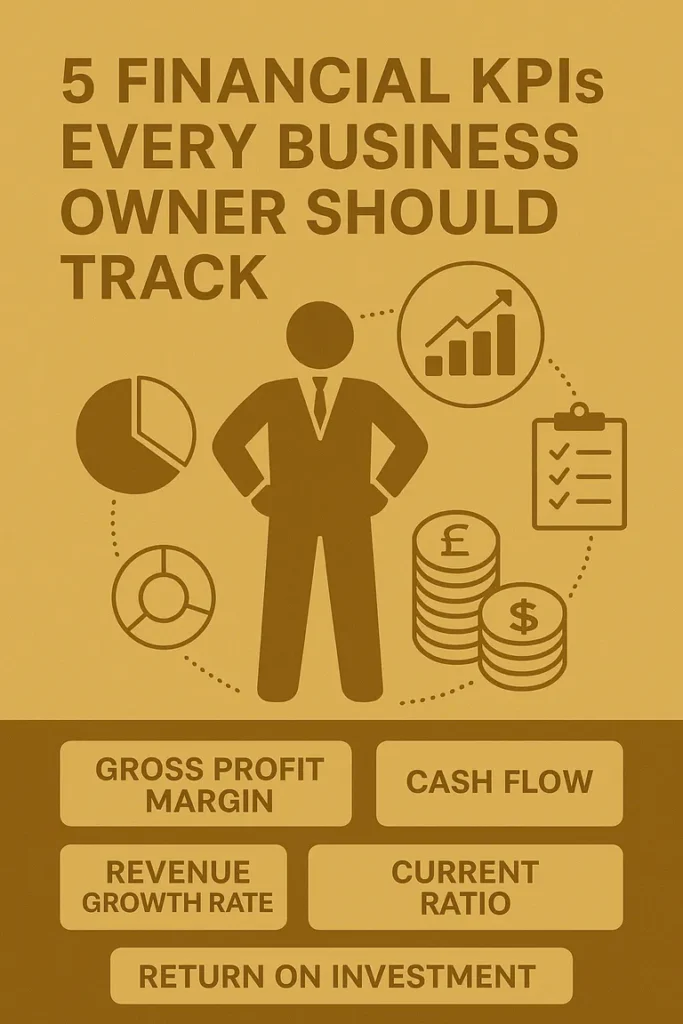

5 Financial KPIs Every Business Owner Should Track

5 Financial KPIs Every Business Owner Should Track Running a successful business requires more than intuition—it requires data-driven decision-making. Financial KPIs (Key Performance Indicators) provide the insight and clarity business owners need to understand performance, improve profitability, and scale with confidence. At Clarus Accountancy Group, we help SMEs monitor the financial metrics that matter most. Here are the five essential KPIs every business owner should be tracking. 1. Gross Profit Margin Gross Profit Margin shows how efficiently your business produces or delivers its products/services. It highlights the relationship between revenue and the direct costs of producing goods (COGS). Formula: (Revenue – Cost of Goods Sold) ÷ Revenue × 100 Why it matters: Reveals product/service profitability Helps identify pricing issues Highlights rising supplier costs Shows where efficiency improvements are needed How Clarus helps: We analyse your cost structure and pricing strategy to ensure sustainable margins. 2. Cash Flow Cash flow measures the net amount of money moving in and out of your business. Even profitable businesses struggle—or fail—due to poor cash flow. Why it matters: Ensures bills, staff, and suppliers are paid on time Allows you to invest confidently Protects against unexpected expenses Provides stability during seasonal fluctuations How Clarus helps: We create real-time cash flow forecasts, automate invoicing, and identify areas to accelerate incoming cash. 3. Revenue Growth Rate Revenue Growth Rate tracks how quickly your business is increasing sales over time. Formula: (Current Period Revenue – Previous Period Revenue) ÷ Previous Period Revenue × 100 Why it matters: Measures business momentum Indicates market demand Helps assess ROI on marketing and sales Supports long-term strategic planning How Clarus helps: We analyse trends using monthly and quarterly data so you can make proactive decisions. 4. Current Ratio The Current Ratio measures your ability to pay short-term liabilities using your short-term assets. Formula: Current Assets ÷ Current Liabilities Why it matters: Indicates financial stability Shows whether you can meet upcoming obligations Helps prevent liquidity crises Healthy range: Typically 1.2–2.0, depending on industry. How Clarus helps: We monitor liquidity levels and advise on steps to maintain healthy working capital. 5. Return on Investment (ROI) ROI evaluates the profitability of a specific investment, such as equipment, marketing, staff, or technology. Formula: (Net Return – Cost of Investment) ÷ Cost of Investment × 100 Why it matters: Identifies where to allocate capital Highlights which marketing channels work Measures the value of operational improvements Helps ensure smart spending that drives growth How Clarus helps: We help calculate ROI across business functions to guide sound investment decisions. ⭐ Final Thoughts Tracking financial KPIs is essential for making informed decisions, improving performance, and scaling sustainably. Whether you’re a start-up or an established SME, the right financial insights can transform the way you run your business. Clarus Accountancy Group provides expert accounting, management reporting, and KPI analysis to help you stay in control and grow confidently.

Why Cash Flow Matters—and How to Improve It Immediately

Cash flow is the lifeblood of every business. You can be profitable on paper and still struggle to survive if cash isn’t flowing when your business needs it. From paying suppliers to funding growth, positive cash flow determines whether your business can operate smoothly—or face unnecessary financial stress. At Clarus Accountancy Group, we help small businesses understand, control, and optimise their cash flow so they can grow with confidence. Here’s why cash flow matters—and the steps you can take to improve it immediately. 1. Cash Flow Determines Your Business’s Financial Health Profit is important, but cash flow is what keeps your business operating day to day. Healthy cash flow ensures you can: Pay suppliers on time Cover payroll and tax obligations Invest in new opportunities Avoid costly emergency loans Weather seasonal dips or unexpected expenses Without strong cash flow, even successful businesses can become vulnerable. 2. Cash Flow Problems Are the #1 Cause of Business Failure Research consistently shows that poor cash flow—not poor sales—is the leading cause of business collapse. Common causes include: Late customer payments Excess stock sitting unsold Rising operating costs Inaccurate forecasting Poor financial management Clarus works with SMEs to identify and resolve these issues early, before they impact business stability. 3. Understanding Cash Flow Helps You Make Smarter Decisions With clear cash flow insight, you can make better choices about: Hiring staff Purchasing equipment Expanding operations Taking on new contracts Managing credit terms When you understand cash flow, you: ✔ Make decisions confidently✔ Avoid unnecessary risk✔ Plan growth without guesswork 4. How to Improve Cash Flow Immediately Here are practical steps any small business can take—starting today. A. Invoice Faster and Automate Payments Slow invoicing = slow cash flow. Improve speed by: Sending invoices immediately Using cloud accounting for automatic invoicing Offering online payment options Automating reminders for overdue invoices This alone can dramatically improve cash flow within weeks. B. Encourage Faster Customer Payments Customers pay faster when it’s easy for them. Try offering: Small discounts for early payment Online card payments Direct debit options Clear payment terms on every invoice C. Review and Reduce Unnecessary Costs Every small saving contributes to healthier cash flow. Assess: Subscriptions you no longer use Suppliers with increasing prices Equipment leases vs. buying Inefficient processes costing time Clarus can help you run a cost-control review that protects your profit margins. D. Improve Stock and Inventory Management Too much inventory = cash trapped on shelves. Reduce stock levels by: Forecasting demand more accurately Switching to just-in-time ordering Clearing old stock Negotiating flexible supply terms E. Negotiate Better Payment Terms If customers pay late but suppliers want early payment, cash flow suffers. Consider: Extending supplier payment terms Reducing customer credit periods Aligning payment cycles with cash inflows F. Build a 3–6 Month Cash Buffer Even a small reserve can protect your business against unexpected costs. This gives you:✔ Stability✔ Security✔ Room for growth Clarus can help you create a cash reserve plan tailored to your business. 5. Cash Flow Forecasting: The Most Powerful Tool You’re Not Using A cash flow forecast is a forward-looking view of your financial position. It helps you see: Future cash shortages When to invest When to cut costs When additional funding is needed Businesses with accurate forecasts grow significantly faster than those without. ⭐ Final Thoughts Cash flow doesn’t have to be complicated—but it must be managed proactively. With expert guidance, automated tools, and smart forecasting, your business can improve cash flow quickly and build long-term financial strength. Clarus Accountancy Group supports small businesses with cash flow management, forecasting, and practical strategies that create financial stability and unlock growth.

How Professional Accounting Helps Scale Your Business Faster

Growing a business is exciting—but scaling sustainably requires more than ambition. It demands visibility, financial clarity, accurate forecasting, and strategic decision-making. This is where professional accounting becomes one of the most powerful growth drivers for small and medium-sized businesses. At Clarus Accountancy Group, we help business owners move beyond reactive bookkeeping into proactive financial management. Here’s how professional accounting accelerates growth and supports long-term scalability. 1. Better Financial Visibility for Smarter Decisions You can’t scale what you can’t measure.Professional accounting gives you clear, real-time insight into: Revenue performance Cash flow trends Profit margins Operating costs Financial risks This level of visibility helps you make informed, strategic decisions rather than reactive ones. How it accelerates growth: ✔ You can identify profitable revenue streams✔ You can eliminate wasteful spending✔ You can confidently invest in new opportunities 2. Strong Cash Flow Management Cash flow problems are the number one reason small businesses fail to scale.With expert accounting, you can: Predict upcoming cash shortages Forecast future cash requirements Ensure invoices are paid on time Plan major purchases Avoid unnecessary borrowing How it accelerates growth: ✔ You maintain financial stability✔ You avoid cash “surprises”✔ You can reinvest in the business at the right time 3. Tax Efficiency That Frees Up More Capital Professional accountants ensure you only pay the tax you owe—nothing more. Clarus helps businesses: Claim every allowable expense Maximise capital allowances Structure director salary/dividends tax-efficiently Access reliefs such as R&D, AIA and creative industry credits Avoid penalties and interest How it accelerates growth: ✔ More retained profit✔ More cash to reinvest✔ Lower financial risk 4. Accurate Forecasting & Budget Planning Scaling requires planning—not guessing. With professional forecasting, you can: Model different growth scenarios Plan for hiring Predict equipment or property needs Understand long-term profitability Build confidence in investment decisions How it accelerates growth: ✔ You know when you can afford to scale✔ You can pitch to investors with confidence✔ You can set measurable targets 5. Helping You Secure Funding Faster Banks and investors need solid, credible financial information.Professional accountants provide: Clean year-end accounts Management reports Cash flow forecasts Business plans and projections Debt and equity guidance How it accelerates growth: ✔ Better chance of loan approval✔ Stronger investor confidence✔ Faster access to capital 6. Streamlined Systems That Save Time Cloud accounting solutions like Xero, QuickBooks, and FreeAgent automate tasks such as: Invoicing Bank reconciliation Expenses VAT returns Payroll How it accelerates growth: ✔ Less admin work✔ Real-time financial data✔ More time to focus on customers and sales 7. Compliance & Risk Reduction Compliance mistakes slow growth, cause stress, and risk penalties. Professional accounting protects your business from: HMRC penalties Incorrect VAT reporting Mismanaged payroll Director loan issues Poor record-keeping How it accelerates growth: ✔ You avoid costly problems✔ You protect your reputation✔ You build a scalable, compliant foundation ⭐ Final Thoughts Professional accounting isn’t just a cost—it’s a strategic investment in faster, safer, and more sustainable business growth. Whether you’re planning to hire, expand, raise finance, or simply improve profitability, the right financial guidance can transform the trajectory of your business. Clarus Accountancy Group provides expert accounting that helps small businesses scale with confidence, clarity, and control.

What Changes in the Latest UK Budget Mean for Small Businesses

The UK’s upcoming Autumn Budget 2025, expected on 26 November, is set to bring a number of shifts that could significantly affect small and medium-sized enterprises (SMEs). Grant Thornton UK+2Debitam+2 At Clarus Accountancy Group, we believe that being ahead of these changes is one of the most important strategic moves a small business owner can make. Here are the key areas you should be watching—and how your business might respond. 1. VAT & Registration Thresholds One of the areas anticipated to see change is the VAT regime for small businesses. Experts suggest that while the headline VAT rate is unlikely to rise, the registration threshold may remain frozen, meaning more businesses will cross the threshold and become VAT-liable. White Oak UK+1What you should do: Review your rolling 12-month turnover to check whether you’re approaching the threshold. Update your bookkeeping and identify whether becoming VAT-registered is beneficial rather than a burden. Speak with Clarus about how VAT registration might impact your pricing, systems and cash-flow. 2. Business Rates Reform Small businesses, especially in retail, hospitality and high-street sectors, are facing reforms to business rates. The government is reportedly looking at “removing cliff-edges” and making reliefs more stable. Reuters+1What you should do: If you occupy premises, review your rateable value and relief eligibility now. Forecast any increases in business rates as part of your budget for next year. Clarus can help you model the impact and plan accordingly. 3. Payroll and Employment Costs With wage inflation, national insurance and minimum wage rises, many small businesses are expecting cost pressures. These changes were flagged ahead of the Budget. White Oak UK+1What you should do: Review your staffing, payroll forecasts, and benefit costs. Consider whether automation or outsourcing (e.g., payroll service) could reduce admin overheads. Speak with Clarus about structuring remuneration (including director salaries/dividends if you’re a limited company) to manage cost. 4. Tax Reliefs & Incentives Budget changes often include adjustments to reliefs, allowances or investment incentives. Although specifics are still to be confirmed, small businesses should prepare. Grant Thornton UKWhat you should do: Review upcoming capital expenditure plans—consider bringing forward asset purchases if that remains tax-efficient. Check whether you’re claiming all applicable reliefs (R&D, investment allowance, etc.). Clarus can review your business’s eligibility for these reliefs and plan ahead. 5. Administrative & Compliance Burdens Ahead of the Budget, a key theme has been reducing red-tape for businesses. For example, the government has signalled a “blitz on bureaucracy” for small firms. The GuardianWhat you should do: Audit your business processes: could you reduce manual entries, streamline bookkeeping or adopt cloud accounting? Ensure your systems are up to scratch—this helps you respond quickly to regulatory changes. Clarus can support you in moving to cloud accounting and improving your internal controls. Final Thoughts The Autumn Budget 2025 may not yet have full details of every measure, but the broad themes are clear: more scrutiny on tax thresholds, cost pressures on employment, reforms to business rates, and a push for greater efficiency in business operations.For small businesses, being proactive is vital: review your financial forecasts, tighten your systems, and seek expert advice now. Clarus Accountancy Group is here to support you every step of the way—from modelling budget impacts to adjusting your business structure and accounting practices.

Common VAT Mistakes

VAT is one of the most common areas where UK businesses make errors—and unfortunately, even a small mistake can lead to penalties, interest charges, or an HMRC investigation. Whether you’re a sole trader, limited company, or growing SME, understanding the most frequent VAT pitfalls can save time, money, and stress. At Clarus Accountancy Group, we help businesses maintain accurate VAT compliance and avoid costly errors. Here are the most common VAT mistakes—and how your business can prevent them. 1. Charging the Wrong VAT Rate The UK has multiple VAT rates, and choosing the wrong one is a frequent source of error. Typical mistakes include: Applying standard rate instead of reduced or zero rate Forgetting to apply VAT to digital services Misapplying VAT on construction or CIS-related work Charging VAT when your business is not yet registered ✔ How to avoid it: Check HMRC’s VAT rate guidelines for your industry Review products/services regularly for correct categorisation Use cloud accounting software with built-in VAT logic Let Clarus Accountancy review your VAT setup 2. Missing VAT Registration or Deregistration Thresholds If your taxable turnover exceeds £90,000 (current threshold), you must register for VAT.Many businesses forget to track this. Common mistakes: Not registering when you pass the threshold Failing to deregister when turnover falls below limit Incorrect estimated turnover forecasting ✔ How to avoid it: Monitor rolling 12-month sales (not your accounting year) Set automatic alerts in your accounting software Ask Clarus to monitor VAT thresholds for you 3. Claiming VAT on Non-Allowable Expenses Not all expenses qualify for VAT recovery. HMRC often rejects: Client entertainment Personal or mixed-use expenses Fuel without proper mileage logs Vehicles used privately International purchases with incorrect VAT treatment ✔ How to avoid it: Keep clear receipts Maintain vehicle mileage records Avoid claiming VAT on entertainment unless rules permit Let your accountant review ambiguous items 4. Errors in VAT Returns Incorrect VAT return figures are among the most common issues. Frequent errors: Duplicated invoices Missing receipts Incorrect box entries Misclassification of zero-rated or exempt sales Not applying reverse charge rules ✔ How to avoid it: Reconcile bank accounts monthly Match invoices to payments Use “check & review” workflows before submission Allow Clarus to prepare or review returns 5. Not Using the Correct VAT Scheme Choosing the wrong VAT scheme can increase admin or cost. Examples: Flat Rate Scheme not suitable Cash Accounting Scheme used incorrectly Annual Accounting Scheme not considered ✔ How to avoid it: Review schemes annually Assess whether a scheme could reduce your VAT bill Get advice from Clarus on the best scheme for your business 6. Late VAT Filing or Payment HMRC penalties can accumulate quickly. Late filing often happens because of: Poor bookkeeping Missing receipts Staff shortages Forgetting deadlines ✔ How to avoid it: Use accounting software reminders Keep books updated monthly Let Clarus handle VAT submissions directly 7. Incorrect VAT on International Sales Cross-border VAT rules are complex and often misunderstood. Mistakes include: Wrong VAT on EU sales Misapplied reverse charge Incorrect place-of-supply rules Missing import/export VAT documentation ✔ How to avoid it: Understand the difference between B2B and B2C VAT rules Apply reverse charge correctly Keep full documentation for imports/exports Seek advice for complex international transactions ⭐ Final Thoughts VAT can be one of the most difficult areas of UK tax compliance—but it doesn’t have to be. With the right systems, professional guidance, and regular checks, your business can avoid penalties and stay confidently compliant. Clarus Accountancy Group offers full VAT support, from registrations and returns to reviewing your VAT scheme and ensuring HMRC compliance. If you need help avoiding VAT mistakes or want your returns professionally managed, we’re here to support you.

How to Prepare for an HMRC Audit: A Practical Guide for SMEs

No business owner enjoys the thought of an HMRC audit—but with the right preparation, the process can be smooth, stress-free, and even beneficial. For many SMEs, an audit simply means HMRC needs to verify that tax returns and financial records are accurate. It does not automatically mean you have done something wrong. At Clarus Accountancy Group, we help businesses prepare for HMRC checks with confidence. This guide breaks down what to expect, how to prepare, and the steps you can take to ensure compliance. What Is an HMRC Audit? An HMRC audit (also called an “HMRC compliance check”) is a formal review of your tax affairs. HMRC may examine: Corporation Tax VAT returns PAYE and payroll Self-assessment returns Business records and bookkeeping Directors’ expenses and dividends Audits may be random, or triggered by specific risk factors such as unusual expenses, inconsistent figures, late filings, or industry-specific compliance issues. 1. Understand Why HMRC Might Contact You HMRC can initiate an audit for several reasons: Common triggers include: Large fluctuations in turnover or expenses Repeated late submissions Missing, incorrect, or inconsistent data High-risk industries (e.g., construction, hospitality) Discrepancies flagged by automated systems Reports from third parties Clarus can help identify potential risk areas before HMRC does. 2. Gather and Organise Your Financial Records The first step in preparing for an audit is ensuring all documentation is accurate and complete. Make sure you have: Full bookkeeping records Sales and purchase invoices Bank statements and reconciliations Payroll records and PAYE submissions VAT records (if registered) Expense receipts Director loan documentation Dividend records and board minutes Cloud accounting software like Xero or QuickBooks makes this much easier and reduces the chance of errors. 3. Review Your Tax Returns for Accuracy Before providing anything to HMRC, double-check all relevant tax returns. Check for: Missing entries Duplicated transactions Unclear descriptions Inconsistent VAT treatment Incorrect expense claims Misreported payroll figures A quick review can prevent small mistakes from becoming bigger issues during the audit. 4. Ensure Your Expense Claims Are Justified HMRC will likely scrutinise business expenses, especially those that may appear “personal.” Make sure expenses are: Wholly and exclusively for business purposes Supported by receipts Clearly categorised Reasonable and consistent Common areas HMRC questions include: Travel and subsistence Home office claims Vehicle expenses Entertainment Director purchases Clarus can help you ensure these are compliant. 5. Check Your VAT Records (If Applicable) VAT inspections are among the most common audits. Ensure: VAT has been applied correctly Partial exemption rules are followed (if relevant) VAT on imports/exports is recorded properly VAT returns match your bookkeeping reports Mistakes in VAT can lead to penalties—so this is an essential review. 6. Review Payroll & PAYE Compliance If you employ staff, HMRC will expect clean, accurate payroll records. Verify that you have: Submitted all RTI (Real Time Information) filings Calculated PAYE and NI correctly Issued P60 and P45 forms Managed employee benefits (P11D) correctly Maintained up-to-date employee records Clarus offers full payroll management if you need hands-off support. 7. Understand What HMRC Will Ask For When HMRC initiates an audit, they will send you a letter explaining what they need. This might include: Specific tax returns Detailed accounts Supporting evidence A face-to-face meeting A meeting at your accountant’s office You have the right to have your accountant communicate with HMRC on your behalf. 8. Cooperate Professionally—but Don’t Overshare Provide exactly what HMRC requests—no more, no less. Do: ✔ Respond promptly✔ Communicate through your accountant✔ Keep records organised✔ Ask for clarification if unclear Don’t: ✘ Offer additional data not requested✘ Guess or estimate figures✘ Delay responses without explanation Clarus can help manage the communication to ensure it stays on track. 9. Minimise Stress by Using Professional Representation An HMRC audit is much easier with an accountant by your side. Clarus can: Communicate directly with HMRC Provide requested records Ensure compliance Correct errors where needed Negotiate penalties (if applicable) Represent you during meetings Professional representation often leads to faster resolutions and fewer complications. 10. Learn From the Audit and Strengthen Your Processes Once the audit is complete, HMRC may: Close the review with no changes Request adjustments Apply interest or penalties (in more serious cases) Use the outcome as a chance to improve your financial systems. Clarus can help you: Strengthen bookkeeping Improve record keeping Automate compliance tasks Implement cloud systems Reduce future audit risk ⭐ Final Thoughts An HMRC audit doesn’t need to be intimidating. With proper preparation, accurate records, and professional support, you can manage the process smoothly and confidently. Clarus Accountancy Group works with SMEs across the UK to ensure compliance, reduce risk, and handle HMRC checks on your behalf—so you can stay focused on running your business.

Your Essential Year-End Tax Checklist for UK Businesses | Clarus Accountancy Group

As the end of the financial year approaches, many business owners begin to feel the pressure of tax deadlines, reporting requirements, and financial housekeeping. At Clarus Accountancy Group, we help UK businesses stay compliant, reduce tax liabilities, and make smarter financial decisions through proactive planning—not last-minute panic. Use this essential year-end tax checklist to stay organised, minimise tax, and enter the new financial year with confidence. 1. Bring Your Bookkeeping Fully Up to Date Clear, accurate records are the foundation of a smooth year-end. Make sure you have: Reconciled all business bank accounts and payment platforms Logged all invoices, bills and receipts Updated expense claims, mileage logs and cash transactions Reviewed payroll reports and staff records If you’re using cloud accounting software like Xero, QuickBooks, or FreeAgent, now is the time to tidy up outstanding balances and correct any discrepancies. 2. Review Outstanding Invoices and Supplier Payments Outstanding invoices can distort your true financial position. Check for: Customers with overdue payments Any debts that should be written off Unprocessed supplier bills Duplicate or incorrect entries Effective credit control improves cash flow—and may reduce your year-end tax bill. 3. Claim All Allowable Business Expenses Many UK businesses lose money each year simply by failing to claim legitimate expenses. Don’t forget: Home office allowances Software, apps and subscription services Professional fees (accountancy, legal, memberships) Training and development Travel and subsistence Marketing and advertising If you’re unsure what you can claim, Clarus can review your spending and ensure you maximise all allowable deductions. 4. Make the Most of Year-End Tax Reliefs and Allowances Before the year closes, take advantage of available reliefs that can significantly reduce your tax bill. Key reliefs include: Annual Investment Allowance (AIA) – 100% relief on qualifying equipment R&D tax credits – even for non-technical businesses that innovate Capital allowances on vehicles, machinery and assets Employment Allowance (if eligible) Pension contributions for directors and employees The right planning can deliver substantial savings. Clarus can guide you through the options relevant to your business. 5. Review Director Salary, Dividends & Pension Strategy For limited companies, this is essential. Consider: Is your director salary tax-efficient? Should you issue dividends before the tax year ends? Are you maximising pension contribution allowances? A well-planned remuneration strategy ensures you pay only what you need to—nothing more. 6. Check Payroll Accuracy and Employee Benefits HMRC can impose penalties if payroll and reporting aren’t correct. Be sure to: Update employee details Reconcile PAYE, National Insurance and pension contributions Review P11D benefits such as vehicles or medical cover Ensure workplace pensions are correctly processed Clarus can manage your payroll to keep your business fully compliant, all year round. 7. Conduct a Stock Take (If Applicable) If your business holds stock, your year-end valuation must be accurate. Review: Slow-moving or obsolete stock Damaged goods Stock write-downs Physical inventory vs recorded inventory Correct stock valuation affects profits, tax liabilities, and financial reporting. 8. Review Cash Flow and Forecast Upcoming Tax Bills Year-end is the ideal moment to step back and assess your financial health. Consider: What tax payments are due in the next 6–12 months? What recurring costs will impact cash flow? Are there seasonal trends you need to factor in? Clarus offers forecasting support to help you plan ahead with clarity. 9. Evaluate Whether Your Business Structure Is Still Right Your current setup might not be the most tax-efficient. Ask yourself: Should I remain a sole trader or become a limited company? Should my business register for VAT (or deregister)? Do we need to restructure ownership or add directors? As your business evolves, your structure should evolve too. 10. Book a Year-End Review With Clarus Accountancy Group A professional review can uncover tax-saving opportunities you may not have spotted. During a year-end consultation, we: Ensure full HMRC compliance Identify tax reliefs and allowances Prepare year-end accounts and tax returns Create a personalised tax planning strategy Support you with bookkeeping, payroll, and VAT Our goal is simple: give you clarity, confidence, and more time to grow your business.